How Does FIDE Function?

In order to understand whether FIDE works efficiently, we conducted a comprehensive analysis of the budget of this organization. Our analysis relied on open data that is published annually by the treasurer. Not being a specialist in finance, I recruited a well-known financial analyst to this work. I’d like to express my sincere gratitude to him. We analyzed the data available for 2009–2018. Before proceeding with the presentation, we had to understand how accurate and correct were the reports published by FIDE.

1. Reporting

In general, the reporting system is striking in its opacity. The reports provided by FIDE shall be accompanied by management reports that shall put the emphasis on the contents. Unfortunately, the current grouping of income and expenditure items does not allow to fully evaluate the efficiency of the FIDE activities and, in particular, its commissions. Data comparison for several years shows the following:

- Income and expenses are deliberately displayed in expanded form, which makes it difficult to assess the real dynamics of income and the direction of use of the funds of the federation.

- Some expenses are deliberately moved to other sections in order to hide the true dynamics of expenses. For example, in the early years, the expenses on the Athens office included payments to Messrs. G. Mastrokoukos and D. Jarret. Now, payments to these people are reflected as consulting expenses.

Correctness of the data presented

We have serious reasons to believe that the reporting provided by FIDE may be misleading. Here are some examples:

- According to the August 2017 letter by the FIDE Executive Director Nigel Freeman, the expenses for the FIDE Deputy President Mr. Makrpopoulos’s travel were 11,625 Euro. At the same time, the FIDE reporting listed the total cost for the business trips of the FIDE Deputy President for the whole of 2017 as just 100 Euro. (It should be noted that the FIDE budget allocated 10,000 Euro for this item.) It remains unclear what was the reason for the incorrect data: whether it was unwillingness to show the true amount of expenses for FIDE officials or the desire to avoid explanations due to overspending in conditions of austerity, when the key chess areas have funding deficits.

- On September 16, 2014, the Russian Chess Federation provided FIDE with a sponsorship in the amount of 100,000 Euro. A proper sponsorship agreement was concluded. In FIDE reporting, this income was not listed under the “sponsorship" heading. Thus, one can question how reliable is all of the data presented - both about FIDE revenues and expenditures.

The questions posed are serious and require at least public explanations from the treasurer and other FIDE decision makers.

Analysis based on available data

Activity dynamics

During eight years since 2009, the FIDE income has grown by 61%. This growth came from increase in fees from the federations and deductions from prize amounts. Other sources of income even decreased during this period.

It should be noted separately that financial expenses of FIDE are significant and ever-growing.

The main beneficiary of income growth is FIDE itself. Regional federations receive almost nothing from the growth of revenues of this structure. On the contrary, they have become net FIDE donors.

While in 2009, the expenses on commissions (considering the income that they earn themselves) and events accounted for 30% of the total budget, in 2017 they were less than 15%!

2014 was tough for FIDE due to significant budget overruns. In 2015, some measures were taken to save budget funds but almost all of them dealt only with spending on commissions and events. The FIDE expenses in this situation continued to grow anyway.

In 2016, cost-cutting activities continued. Expenses for commissions and activities were reduced two more times. The expenses of the federation itself were cut only by 25%.

In 2017, cost-cutting activities continued as well. However, the reductions were only achieved in spending on commissions and events. The net expenses for the work of commissions in 2017 will amount to less than FIDE lost during the year on financial transactions!

In general, one can conclude that FIDE spends about 85% of its budget on its own structures!

More questions that have to be asked about this regrettable situation:

- Why is not FIDE looking for other sources of funding?

- Why there is no movement towards putting its activities on a business footing? The FIDE carries a budget deficit – why does it "forgive" the debt to AGON to the tune of 500.000 Euro?!

How the data was analyzed:

Income

In the table below, the revenues are shown in a balanced form, i.e. income minus the cost to generate / earn it. The reasoning: These are forced costs. By decreasing our revenues immediately by these amounts, we show how what funds were actually at FIDE’s disposal.

• “Commissions”. Income from this line item has been reduced by the amount of early payment discounts and the write-off of the income that was previously recorded but not received. This is even more relevant since FIDE has planned to increase contributions. The reasoning: What is the point in raising contributions if discounts will be given to those who paid in advance whereas the debts of those who had the means to pay but did not will be written off anyway. As a result, income growth will be less than planned.

• I made "Commercial activity" a separate item. It is comprised of royalties and sponsorships. Previously, they were included in Other income. The reasoning: Sport is being commercialized so royalties and sponsorships became one of main sources of income for sports federations and teams around the world.

• I made “Results from financial activities” a separate item. This is a highly specialized item which comprises results from the FIDE fund management, revaluation of securities and foreign currencies, and bank charges. Basically, it was a transfer of expenses. The reasoning: Revaluations reduce the amount of funds at the federation’s disposal; bank charges also reduce the assets available. The FIDE bears the expenses but receives nothing in return. These are issues for the Treasurer, not for the whole federation.

• Revenues from commissions were excluded from the revenue part and transferred to the expenditure side. The reasoning: Commissions’ activity generates income. It is logical to dedicate this income to financing those same activities, then to top up the deficit if any. In this case, the FIDE’s financial contribution to the work of its commissions would be immediately visible. In addition, only the income affected by the decisions of the FIDE administration would show in the total amount of income.

• Taxes were also shown as a decrease in revenue. The reasoning: Calculate how much money remains at FIDE's disposal to carry out its activities.

Bottom line: the actual amount of funds that FIDE has at its disposal is somewhat less than the official reporting shows.

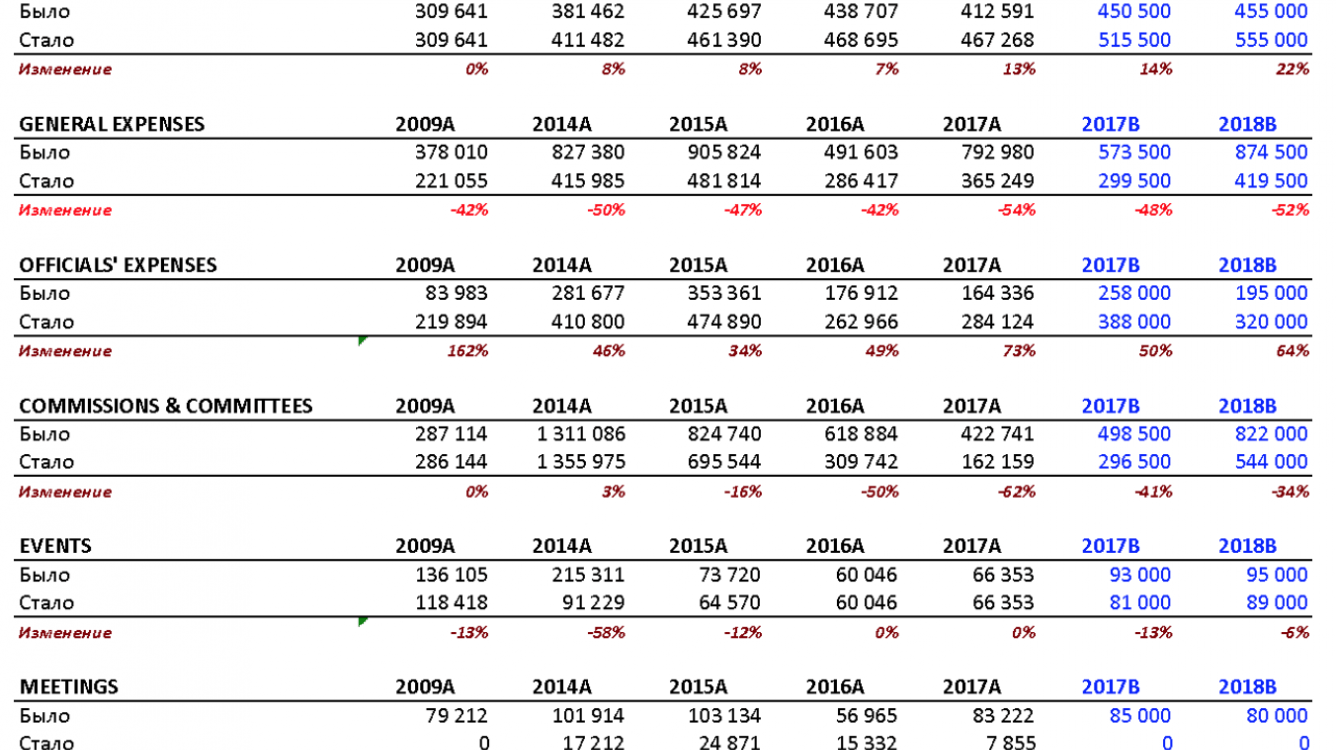

Costs

The reasoning behind the regrouping of expenses that we undertook was to show first of all what was the money spent on, and then to demonstrate how.

•“Expenses on the Athens office”. This item included the payments to consultants. The reasoning: G.Mastrokoukos (the owner of Itwebia) and D.Jarret have worked in FIDE previously, then left, and the new expense item appeared. One suspects that this was simply a conversion of internal expenses into external ones.

• We created a new item called "Expenses on other FIDE offices". The expenditures on Moscow and Elista offices were totaled there.

• The item “Expenses on FIDE officials” was supplemented with expenses on insurance and for organizing Presidential Board meetings. One the accompanying notes stated that in a certain year, FIDE managed to achieve savings on insurance due to the fact that it no longer covered insurance for the congress delegates. However, the federation pays for insurance of its staff, its management and key commission members. The reasoning: It is the FIDE that chooses to pay for insurance, it is at the request of FIDE board members that meetings are held in person – thus, such expenses are discretionary and it would be correct add them to the expenses on FIDE management.

• “Expenses on commissions” are shown as expenditures in a balanced form. The reasoning was explained above.

• "General expenses". The following expenditures were excluded from this category and transferred to others: "Taxes", "Write-offs", "Revaluations", "Consultants", "Insurances", "Expenses on Agon", "Refunds on Contributions".

• "Competitions". The competitions financed from the commissions’ budgets were transferred to the commissions’ expenses.

• “Meetings”. The item of expenditure was split into expenses on congresses and expenses on the Presidential Board / the Executive Board. The latter were transferred to the expenses on FIDE officials.

Results achieved:

• Expenses for “the common good”, a.k.a. general expenses, were reduced significantly: either by transferring the expenditures that were not true expenditures, or by transferring the costs incurred by the FIDE apparatus into the appropriate sections.

• Targeted expenses have increased.

In general, one can conclude that FIDE spends about 85% of its budget on its own structures!

Conclusions:

1. FIDE reporting is at the very least incorrect. Such egregious examples as missing reporting of the 2014 RCF sponsorship contract and the disappearing 2017 travel expenses of the deputy president show that FIDE needs a full-fledged audit.

2. Even according to published data, it is clear that FIDE spends more than 80 percent of its budget on its own management. In this situation, it is necessary to look for new sources of funding. At the moment, the contributions from the national federations are practically the only lifeline that ensures FIDE’s existence. At the same time, the development budget is reduced every year; the decrease was almost 50 percent compared to 2014.

3. The only commercial contract that FIDE has – that with Agon - is not observed or is only partially observed. This contract is non-public and does not serve FIDE’s interests.

4. The current FIDE leadership is not able to find alternative funding sources that are customary for successful international sports organizations.